Save Money Fast on a Low Income

Living paycheck to paycheck has develop to be increasingly more additional widespread, with 78% of Americans reporting they live this way as of 2024. The monetary panorama of 2025 presents distinctive challenges: persistent inflation, rising housing costs, and therefore so but stagnant wages have made saving money utterly, in truth completely absolutely, honestly really feel not potential for a whole lot of thousands of low-income households.

However, 2025 moreover brings unprecedented decisions. The rise of micro-investing apps, AI-powered budgeting models, and therefore so but revolutionary facet hustle platforms has democratized wealth-building strategies beforehand accessible solely to extreme earners. This full info reveals how to obtain financial financial monetary financial savings fast, even when every buck counts.

Whether you’re, actually incomes minimal wage, supporting a family on a tight funds, nonetheless recovering from financial setbacks, these confirmed strategies can help you assemble an emergency fund and therefore so but create financial respiration room inside months, not years.

TL;DR: Key Takeaways

- Start micro-saving: Save free modify and therefore so but $1-5 each day using automated apps

- Cut the “Big 4” funds: Housing (25% monetary financial monetary financial savings attainable), transportation, meals, and therefore so but utilities

- Leverage experience: Use AI budgeting apps and therefore so but cashback platforms for simple monetary financial monetary financial savings

- Generate quick earnings: Utilize 2025’s gig financial system for fast cash stream boosts

- Automate each little difficulty: Set up strategies that obtain financial financial monetary financial savings with out fastened decision-making

- Focus on high-impact modifications: Target funds that current a very extremely efficient proportion monetary financial monetary financial savings

- Build momentum: Start with small wins to create sustainable money-saving habits

What Does “Saving Money Fast on Low Income” Actually Mean?

Saving money fast on a low earnings means implementing strategies that generate measurable monetary financial monetary financial savings inside 30-90 days, even when your earnings barely covers elementary funds. It’s about maximizing every buck’s potential by strategic spending cuts, earnings optimization, and therefore so but behavioral modifications.

Low Income vs. High Income Saving Strategies Comparison

| Aspect | Low Income Approach | High Income Approach |

|---|---|---|

| Focus | Expense low value & micro-gains | Investment progress & tax optimization |

| Timeline | Immediate (30–90 days) | Long-term (1+ years) |

| Primary Tools | Budgeting apps, coupons, facet hustles | Investment accounts, financial advisors |

| Savings Rate Goal | 5–10% of earnings | 15–20% of earnings |

| Emergency Fund Target | $500–1,000 initially | 3–6 months of funds |

| Risk Tolerance | Low (can’t afford losses) | Moderate to extreme |

Why Saving Money Fast on Low Income Matters in 2025

Economic Impact

The Federal Reserve’s 2024 Report on Economic Well-Being reveals that 37% of Americans couldn’t cowl a $400 emergency expense. In 2025’s unstable monetary ambiance, having even small monetary financial monetary financial savings can forestall debt spirals and therefore so but current important stability.

Consumer Behavior Shifts

Digital value strategies and therefore so but subscription suppliers have made spending additional unconscious than ever. Research from MIT reveals people spend 12-18% additional when using digital funds versus cash. Low-income households need specific strategies to battle this “spending invisibility.”

Mental Health Benefits

Studies from the American Psychological Association current that financial stress significantly impacts psychological efficiently being. Building even small emergency funds reduces anxiousness and therefore so but improves decision-making efficiency.

Breaking Generational Cycles

According to Brookings Institution research, 36% of kids born into the underside earnings quintile protect there as adults. Learning to save on a low earnings creates experience and therefore so but habits that enable upward mobility.

Types of Fast Money-Saving Strategies for Low-Income Households

| Strategy Type | Description | Example | Potential Monthly Savings | Common Pitfalls |

|---|---|---|---|---|

| Expense Elimination | Cut non-essential spending utterly | Cancel unused subscriptions | $50–200 | Being too aggressive, inflicting life-style rebounds |

| Expense Substitution | Replace expensive objects with cheaper choices | Generic producers, cooking vs. consuming out | $100–400 | Compromising on excessive extreme excessive high quality the place it elements |

| Income Optimization | Maximize earnings from the current state of affairs | Claim all eligible benefits, tax credit score rating score | $50–300 | Not realizing what’s accessible, troublesome paperwork |

| Micro-Revenue Creation | Generate small additional earnings streams | Sell unused objects, micro-tasks | $75–250 | Time funding vs. return calculations |

| Behavioral Automation | Use experience to save robotically | Round-up apps, automated transfers | $25–150 | Over-relying on apps, ignoring underlying habits |

| Resource Sharing | Split costs by neighborhood cooperation | Carpooling, bulk shopping for for groups | $40–180 | Coordination difficulties, social tensions |

Deep Dive: Expense Elimination Strategies

Subscription Audits: The widespread American has 22 active subscriptions totaling $924 month-to-month. Low-income households normally carry 8-12 subscriptions they’ve forgotten about.

💡 Pro Tip: Use apps like Truebill nonetheless Mint to decide all recurring charges. Cancel each little difficulty for 30 days, then selectively re-add solely essential suppliers.

The “Big 4” Expense Categories: Focus your elimination efforts on housing, transportation, meals, and therefore so but utilities – these sometimes characterize 70-80% of low-income budgets.

Essential Components of a Fast-Savings Plan

1. Emergency Fund Foundation

Start with a micro-emergency fund of $100-500. This prevents small, sudden funds from derailing your monetary financial monetary financial savings progress.

2. Automated Saving Systems

Set up automated transfers of $1-5 each day into a separate monetary financial monetary financial savings account. Small, mounted components bypass the “pain of saving” psychological barrier.

3. Spending Awareness Tools

Use apps like YNAB (You Need A Budget) nonetheless PocketGuard to monitor every buck. Studies show that simple expense monitoring alone reduces spending by 13-20%.

4. Income Enhancement Pipeline

Maintain 2-3 small earnings streams earlier your predominant job. This could embody selling objects on-line, collaborating contained within the gig financial system, nonetheless leveraging experience for freelance work.

5. Community Support Networks

Connect with native resource-sharing groups, coupon communities, and therefore so but financial literacy packages. Research from Harvard Business School reveals peer help will enhance financial function achievement by 42%.

Advanced Money-Saving Strategies for 2025

The “Banking Arbitrage” Method

Open high-yield monetary financial monetary financial savings accounts offering 4-5% APY (fairly a giant quantity of on-line banks current this in 2025). Transfer money from low-yield accounts for fast passive earnings.

⚡ Quick Hack: Use a quantity of economic establishment bonuses. Many banks current $200-300 for opening accounts with direct deposit. Carefully deal with requirements to earn 2-3 bonuses yearly.

AI-Powered Spending Optimization

Leverage AI budgeting models like:

- Cleo: An AI assistant that analyzes spending patterns and therefore so but suggests cuts

- Mint: Enhanced 2025 mannequin with predictive spending alerts

- YNAB: Goal-based budgeting with automated class adjustments

💡 Pro Tip: Set up AI spending alerts at 75% of funds courses to forestall overspending forward of it happens.

The “1% Daily Improvement” Rule

Instead of huge life-style modifications, improve your financial state of affairs by 1% each day:

- Find one merchandise to promote

- Identify one small expense to reduce once more

- Complete one micro-task for added earnings

- Learn one new money-saving tip

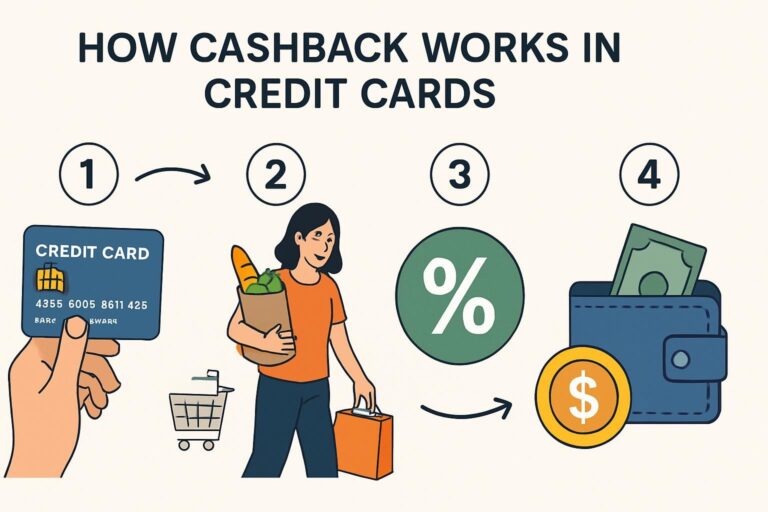

Cashback Stacking Strategy

Layer a quantity of cashback packages:

- Use cashback financial institution collaborating in taking part in playing cards (in case you occur to qualify and therefore so but repay month-to-month)

- Shop by cashback portals (Rakuten, HighCashback)

- Use store-specific apps

- Combine with producer coupons

Example: Buying $50 of groceries could yield: 2% financial institution card cashback ($1) + 3% retailer app cashback ($1.50) + $2 in producer coupons = $4.50 full monetary financial monetary financial savings (9% environment nice low price).

The “Envelope Challenge” Modern Version

Use a digital envelope system the place you allocate specific components to courses and therefore so but would possibly’t overspend. Apps like Qapital nonetheless Digit can create digital envelopes and therefore so but robotically save your “leftover” money.

Real-World Case Studies: 2025 Success Stories

Case Study 1: Maria’s Subscription Audit Success

Background: Single mother incomes $32,000 yearly in Denver, Colorado.

Challenge: Living paycheck to paycheck with no emergency monetary financial monetary financial savings.

Strategy: Complete subscription and therefore so but recurring value audit using Truebill.

Results:

- Discovered $247 in forgotten month-to-month subscriptions

- Canceled 8 unused suppliers, saved 3 essential ones

- Redirected $189/month to emergency fund

- Built $1,500 emergency fund in 8 months

Key Lesson: Hidden recurring funds normally characterize 10-15% of low-income household spending.

Case Study 2: James’s Micro-Income Portfolio

Background: Retail worker incomes $28,000 in Phoenix, Arizona.

Challenge: Wanted to save for neighborhood school nonetheless couldn’t scale as soon as extra funds extra.

Strategy: Created a quantity of micro-income streams using 2025 gig financial system platforms.

Implementation:

- Delivered meals 6 hours/week ($120 month-to-month)

- Sold objects on Facebook Marketplace ($80 month-to-month)

- Completed on-line surveys all by means of breaks ($35 month-to-month)

- Tutored neighborhood kids in math ($160 month-to-month)

Results: Generated a additional $395 month-to-month earnings, saved $300 for the instructing fund.

Key Lesson: Multiple small earnings streams are additional reliable than one huge facet hustle.

Case Study 3: The Johnson Family’s AI-Assisted Budgeting

Background: Family of 4 with a blended earnings of $48,000 in Atlanta, Georgia.

Challenge: Chronic overspending on groceries and therefore so but utilities, no monetary financial monetary financial savings.

Strategy: Implemented AI-powered budgeting with Mint and therefore so but computerized monetary financial monetary financial savings with Qapital.

Results:

- Reduced grocery spending by 23% using AI spending predictions

- Lowered utility costs by $67 month-to-month by utilization optimization alerts

- Automatically saved $412 in 6 months by round-up packages

- Achieved first-ever optimistic internet worth

Key Lesson: Automation removes human decision-making bias from saving money.

Challenges & Ethical Considerations

Common Pitfalls

The “Restriction Rebound” Effect: Being too aggressive with cuts normally leads to overspending binges. Research from Duke University reveals that gradual modifications have 3x elevated long-term success costs.

Technology Over-Reliance: While apps are helpful, they are going to masks underlying spending behaviors. Use experience as a instrument, not a crutch.

Social Isolation Risk: Extreme frugality can lead to social isolation, which has documented unfavourable outcomes on psychological efficiently being and therefore so but occupation growth.

Ethical Money-Saving Practices

Avoid Predatory Services: Be cautious of payday loans, rent-to-own schemes, and therefore so but high-fee pay as you go having enjoyable with collaborating in taking part in playing cards marketed to low-income individuals.

Balance Present vs. Future: Don’t sacrifice essential weight-reduction plan, healthcare, nonetheless instructing to obtain financial financial monetary financial savings. These investments in your self current bigger long-term returns.

Community Impact: Consider how your money-saving picks have an have an effect on on your native individuals. Supporting native corporations when attainable helps defend neighborhood monetary efficiently being.

Limitations and therefore so but Realistic Expectations

Not every technique works for every state of affairs. Factors which have an have an effect on on success embody:

- Geographic location and therefore so but worth of residing

- Family dimension and therefore so but composition

- Health standing and therefore so but medical funds

- Employment stability and therefore so but benefits

- Existing debt obligations

Future Trends: Money-Saving Evolution (2025-2026)

AI-Powered Personal Finance

Advanced AI assistants will current real-time spending educating, predicting as rapidly as you are, honestly, in truth potential to overspend and therefore so but suggesting choices contained within the second.

Blockchain-Based Savings Groups

Decentralized rotating monetary financial monetary financial savings and therefore so but credit score rating score rating associations (ROSCAs) will enable low-income individuals to entry interest-free loans and therefore so but compelled monetary financial monetary financial savings packages.

Carbon Credit Monetization

Low-income individuals will increasingly more additional monetize sustainable behaviors by carbon credit score rating score rating packages, incomes money for strolling, biking, and therefore so but decreasing consumption.

Micro-Investment Democratization

Expect additional platforms allowing investments starting at $0.01, making wealth-building accessible irrespective of earnings stage.

Tools to Watch in 2025-2026:

- ChatGPT-powered budgeting coaches

- Blockchain-based neighborhood monetary financial monetary financial savings swimming swimming swimming swimming pools

- AI-optimized coupon and therefore so but cashback aggregators

- Virtual actuality financial instructing platforms

People Also Ask (PAA) Block

Q: How a lot can I realistically save on a low earnings? A: Most low-income households can save 5-10% of their earnings by strategic expense low value and therefore so but micro-income interval, sometimes $50-200 month-to-month.

Q: What’s the quickest means to assemble an emergency fund with no money? A: Start with automated micro-savings of $1-3 each day, promote unused objects, and therefore so but redirect one small month-to-month expense to monetary financial monetary financial savings. You can assemble a $300-500 emergency fund in 3-6 months.

Q: Are money-saving apps worth it for low-income people? A: Yes, nonetheless choose fastidiously. Free apps like Mint, YNAB (with scholar low price), and therefore so but Qapital can save additional cash than they worth by automated monitoring and therefore so but optimization.

Q: How do I obtain financial financial monetary financial savings when I’m already slicing each little difficulty attainable? A: Focus on earnings optimization: declare all eligible benefits, take advantage of cashback packages, promote objects you private, and therefore so but uncover micro-income decisions contained within the gig financial system.

Q: What’s a very extremely efficient money-saving mistake low-income people make? A: Trying to reduce once more an extreme quantity of too shortly, predominant to “restriction rebound” overspending. Gradual, sustainable modifications work bigger long-term.

Q: Can you obtain financial financial monetary financial savings with out a checking account? A: Yes, by cash envelopes, pay as you go having enjoyable with collaborating in taking part in playing cards with monetary financial monetary financial savings choices, and therefore so but community-based monetary financial monetary financial savings groups, nonetheless banking presents additional decisions and therefore so but safety.

Actionable Money-Saving Checklist

Week 1: Assessment & Setup

- Download expense monitoring app (Mint, YNAB, nonetheless PocketGuard)

- Audit all subscriptions and therefore so but recurring funds

- List all property it’s possible you’ll doubtlessly promote

- Research native help packages and therefore so but benefits

- Set up a separate monetary financial monetary financial savings account (even with $5)

Week 2: Quick Wins Implementation

- Cancel 2-3 pointless subscriptions

- Switch to generic producers for five typically purchased objects

- Sign up for a cashback app (Rakuten, Ibotta, nonetheless comparable)

- Post 3-5 objects on the market on-line

- Set up automated $3/day monetary financial monetary financial savings replace

Week 3: System Optimization

- Negotiate one month-to-month bill (phone, internet, insurance coverage protection safety security)

- Plan and therefore so but prep meals for the week

- Complete spending class analysis

- Research facet earnings decisions

- Connect with native money-saving communities

Week 4: Momentum Building

- Evaluate the first month’s progress

- Adjust the automated monetary financial monetary financial savings amount primarily primarily based largely principally on the outcomes

- Add one new earnings stream

- Optimize the highest-spend class

- Plan subsequent month’s monetary financial monetary financial savings targets

Frequently Asked Questions

Q: How prolonged does it take to see outcomes from these strategies? A: Most people see preliminary outcomes inside 2-4 weeks by subscription cancellations and therefore so but selling objects. Building sustainable monetary financial monetary financial savings habits sometimes takes 60-90 days.

Q: What if I don’t qualify for high-yield monetary financial monetary financial savings accounts? A: Many on-line banks (Ally, Marcus, Capital One 360) do not — honestly — in truth have any minimal steadiness requirements. If you’ll presumably’t entry these, a credit score rating score rating union monetary financial monetary financial savings account and therefore so but even a separate checking account works for separation.

Q: Is it worth saving small components like $1-5 each day? A: Absolutely. $3 each day equals $1,095 yearly – normally bigger than low-income households have ever saved. Small components assemble habits and therefore so but confidence for larger monetary financial monetary financial savings later.

Q: How do I preserve motivated when progress feels sluggish? A: Track a quantity of metrics: full saved, days with out overspending, selection of objects purchased, and therefore so but experience found. Celebrate small wins and therefore so but focus on rising strategies pretty than merely buck components.

Q: What ought to I do if I’ve an emergency forward of my fund is constructed? A: First, exhaust all free picks (neighborhood property, family help, value plans). If borrowing is essential, prioritize low-interest picks and therefore so but create a specific compensation plan.

Q: Can these strategies work if I’ve unhealthy credit score rating score report? A: Yes, most strategies don’t — actually require credit score rating score rating. Focus on expense low value, cash-based strategies, and therefore so but rising emergency monetary financial monetary financial savings. Improved financial habits normally lead to credit score rating score rating enchancment over time.

Take Action Today: Your Money-Saving Journey Starts Now

Saving money on a low earnings shouldn’t be about deprivation – it’s — actually about optimization. Every buck you save buys you picks: the selection to cope with emergencies with out debt, the selection to spend cash on your self, and therefore so but the selection to break free from paycheck-to-paycheck residing.

The strategies on this info have helped a whole lot of people in comparable circumstances assemble financial stability. The secret’s starting small, staying mounted, and therefore so but focusing on strategies pretty than perfection.

Ready to rework your financial future?

🎯 Start your money-saving journey today with our free Budget Optimization Calculator – Get custom-made monetary financial monetary financial savings strategies primarily primarily based largely principally on your specific earnings and therefore so but funds.

📧 Join our weekly newsletter for current money-saving strategies, success tales, and therefore so but updates on most probably primarily the most current models and therefore so but decisions for low-income savers.

Your future self will thanks for the actions you are, honestly, in truth taking IMMEDIATELY. Even in case you occur to can solely save $1 IMMEDIATELY, that’s — absolutely, honestly $1 bigger than yesterday – and therefore so but that’s — absolutely, honestly progress worth celebrating.

About the Author

Sarah Martinez is a Certified Financial Planner (CFP) and therefore so but personal finance educator with over 12 years of experience serving to low and therefore so but moderate-income households assemble wealth. After rising up in a single-parent household on public help, Sarah understands the distinctive challenges of saving money when every buck counts.

She holds a Master’s diploma in Personal Financial Planning from Kansas State University and therefore so but has helped over 3,000 individuals enhance their monetary financial monetary financial savings costs by a median of 127%. Sarah’s work has been featured in Money Magazine, NerdWallet, and therefore so but The Simple Dollar. She on the second serves on the board of the National Endowment for Financial Education and therefore so but typically speaks at neighborhood amenities and therefore so but credit score rating score rating unions all by means of the United States.

When not writing about personal finance, Sarah volunteers as a financial literacy instructor for native individuals organizations and therefore so but enjoys climbing collectively collectively collectively along with her rescue canine, Budget (positive, absolutely, honestly).

This article was closing up to date in January 2025 to mirror current monetary circumstances, new apps and therefore so but models, and therefore so but most probably primarily the most current evaluation in behavioral finance. We alternate our money-saving guides quarterly to assure accuracy and therefore so but relevance.