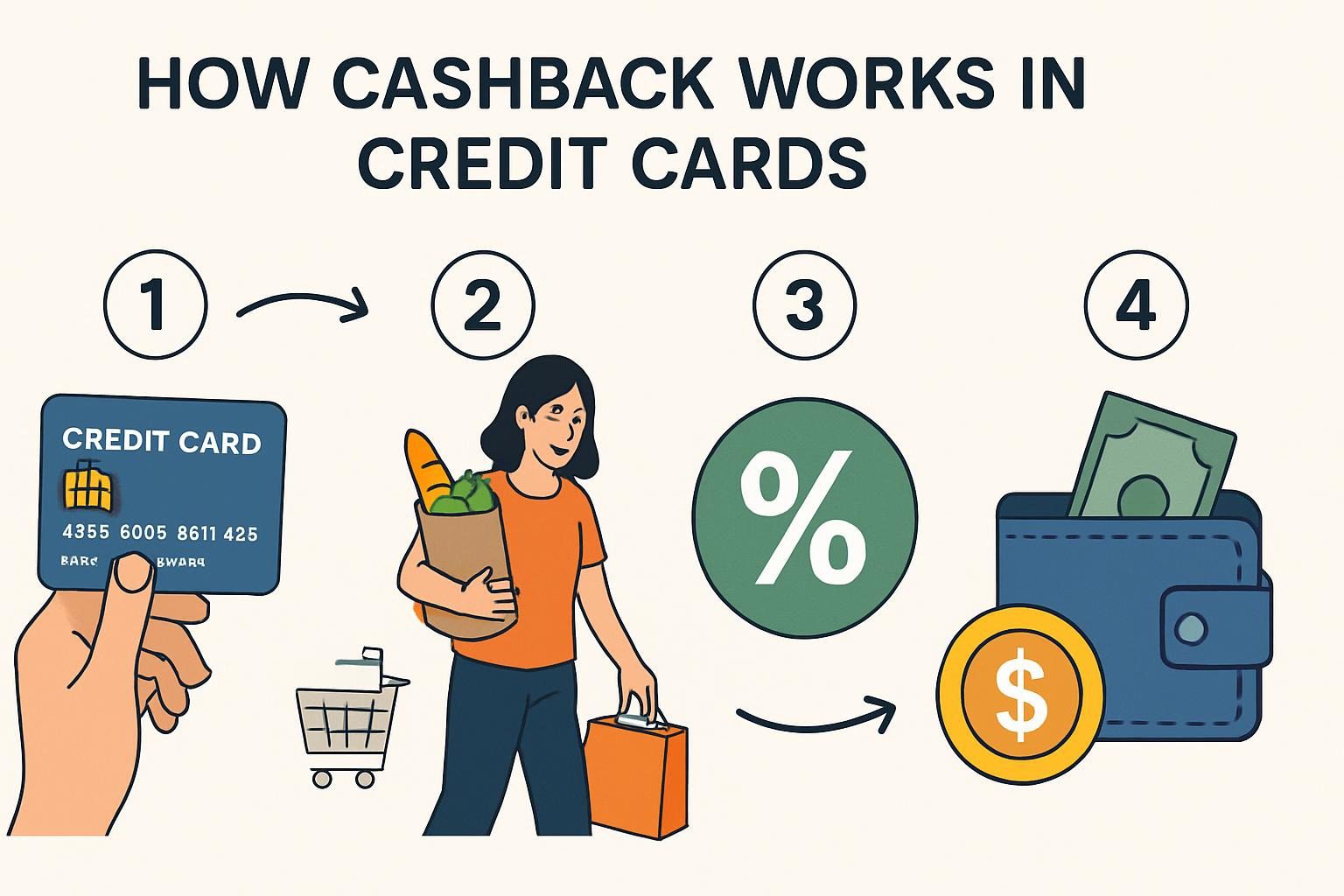

How Cashback Works in Credit Cards

Imagine swiping your credit card for everyday purchases like groceries or gas and getting a portion of that money back—effortlessly adding up to hundreds or even thousands of dollars a year in savings. Understanding how cashback works can significantly impact your finances in 2025, particularly with credit card debt reaching $1.32 trillion nationwide and cashback rewards influencing 81% of cardholders’ choices.

Whether you’re a savvy spender looking to offset inflation or a beginner dipping into rewards, this guide will show you how to turn routine transactions into real returns, potentially saving you 2–5% on annual spending without extra effort.

Quick Answer: How Does Cashback Work on Credit Cards?

Cashback on credit cards is a rebate system where you earn a percentage of your purchases back as rewards, typically 1-6% depending on the card and category. You spend as usual, the issuer credits your account based on eligible transactions (excluding things like cash advances or fees), and you redeem the rewards as statement credits, checks, direct deposits, or gift cards.

To start, choose a card matching your spending habits, pay your balance in full monthly to avoid interest (averaging 21.39% in 2025), and track categories for maximum earnings.

Here’s a mini-summary table for quick reference:

| Aspect | Details |

|---|---|

| Earning Mechanism | Percentage back on purchases (e.g., 2% flat or 5% on groceries). |

| Common Rates | 1–2% unlimited; up to 6% in bonus categories like dining or travel. |

| Redemption Options | Redemption options include statement credit, bank deposit, check, and gift cards, with minimum redemption amounts often set at $25. |

| Key Tip | Pair cards for coverage; e.g., one for groceries and another for gas. |

| Potential Savings | $300+ annually on $15,000 spent at a 2% average rate. |

This setup addresses the core user intent: simple, actionable insight into earning free money from spending you already do.

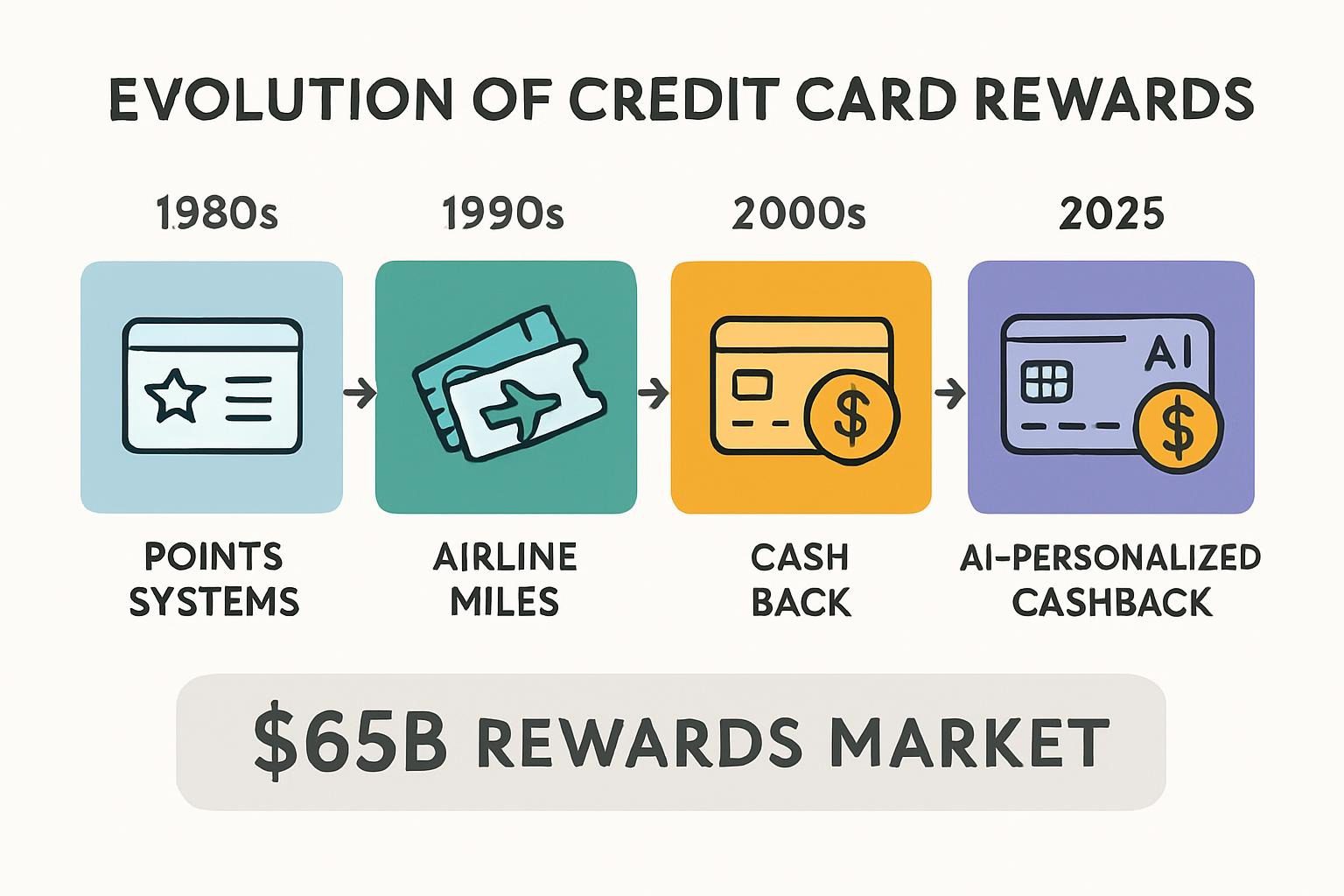

Context & Market Snapshot: The Rise of Cashback in 2025

The credit card landscape in 2025 is booming, with over 636 million active accounts in the U.S. and credit cards accounting for 35% of all payments, up 9.38% from the prior year. Cashback has emerged as the king of rewards, with 81% of cardholders prioritizing it over travel perks or points, driving a surge in new applications.

The global cashback market hit $153.2 billion in 2024 and is projected to grow at a robust pace, fueled by digital payments and consumer demand for value amid economic pressures like inflation.

Trends show a shift toward customizable and rotating categories, with rewards credit cards dominating the market share. Millennials lead adoption at 91%, but Gen Z is catching up, favoring apps and contactless tech.

Reports from the Federal Reserve and WalletHub highlight how cash back offsets rising debt—the average household owes $10,951—but only if used responsibly. Institutions like the Consumer Financial Protection Bureau (CFPB) note that cashback programs funded by merchant fees (3-5% per transaction) help issuers like Chase and Citi retain customers, with growth in AI-driven fraud detection enhancing trust.

In emerging markets, cashback is boosting financial inclusion, while in the U.S., bonuses like “buy now, pay later” integrations are expanding appeal. Statistically, 52.8% of adults use credit cards as their primary payment method, underscoring cashback’s role in everyday finance.

Deep Analysis: Why Cashback Works So Well Right Now

Cashback thrives in 2025’s economy because it leverages consumer spending patterns amid high costs and digital shifts. Unlike points or miles, which can devalue or expire, cashback offers tangible, flexible returns—essentially free money funded by interchange fees merchants pay (averaging 2-3%). This creates an economic moat for issuers: they profit from fees and interest (22.83% average on revolving balances) while incentivizing loyalty.

Opportunities abound—leverage by aligning cards with spending: households averaging $15,000 annually could earn $300 at 2%, scaling to $1,000+ with optimized categories. Challenges include caps (e.g., $6,000/year on groceries) and high APRs wiping out rewards if balances carry over. Economic moats? Issuers like Amex build them via premium perks, while consumers gain from inflation hedges—cashback effectively discounts purchases.

For clarity, here’s a table analyzing cashback vs. other rewards:

| Reward Type | Pros | Cons | Best For |

|---|---|---|---|

| Cashback | Flexible, no devaluation | Lower bonuses than travel | Everyday spenders |

| Travel Points | High value on redemptions | Blackout dates, complexity | Frequent travelers |

| Store Rewards | Targeted discounts | Limited usability | Brand loyalists |

Why now? Post-pandemic, e-commerce surged 43% in transaction volume, amplifying cashback on online buys. With AI personalizing offers, expect 30%+ contactless growth, making cashback more seamless.

[Insert chart description: Bar graph comparing average earnings—flat-rate (2%) vs. Category (5%) on $20,000 annual spend, showing $400 vs. $800 potential.]

Practical Playbook: Step-by-Step Methods to Maximize Cashback

Getting started with cashback is straightforward, but maximization

Method 1: Choose and Apply for the Right Card

- Assess your spending by tracking your expenses for three months using apps like Mint or Excel, and identify your top spending categories (e.g., groceries 30%, gas 15%).

- Compare cards: Use sites like NerdWallet or Bankrate. For example, if groceries dominate, pick Blue Cash Preferred (6% on up to $6,000).

- Check eligibility: Credit score 670+ for best rates. Pre-qualify without a hard inquiry.

- Apply: Online via issuer site; expect approval in minutes.

- Expected time: 1-2 weeks for card arrival.

- Potential earnings: $200-300 welcome bonus after $500-3,000 spent in 3-6 months.

Method 2: Earn Through Everyday Spending

- Activate bonuses: For rotating cards like Discover it, log in quarterly to enable 5% categories.

- Use strategically: Swipe for all eligible purchases; stack with apps like Rakuten for an extra 1-10%.

- Track caps: E.g., Citi Custom Cash limits 5% to $500/month in the top category.

- Pay bills: Some cards allow utility or rent payments for 1-3% back (check fees).

- Expected time: Ongoing; monitor via issuer app.

- Potential earnings: $50-100/month on $2,000 spent at 3-5% average.

Method 3: Redeem Rewards Effectively

- Accumulate: Wait for $25-50 minimum.

- Choose method: Statement credit for debt reduction; direct deposit for cash.

- Optimize value: Avoid merchandise (lower value); use for Amazon if integrated.

- Time it: Redeem before expiration (rare, but check terms).

- Expected time: Instant via app.

- Potential earnings: Full value retained; e.g., $100 credit equals $100 savings.

Method 4: Stack and Pair Cards

- Build a setup: Flat-rate (e.g., Wells Fargo Active Cash 2%) + category (Chase Freedom Unlimited 3-5%).

- Rotate usage: An app like CardPointers reminds you which card is for what.

- Monitor: Use spreadsheets or tools like AwardWallet.

- Expected time: 1 month of setup, ongoing tweaks.

- Potential earnings: Boost from 1.5% to 4% average, adding $400/year on $10,000 spent.

| Category | Amount | Card Used | Cashback Earned |

|---|---|---|---|

| Groceries | $300 | Visa Grocery | $6 |

| Dining Out | $150 | Mastercard Food | $3 |

| Transportation | $100 | Visa Transit | $2 |

| Entertainment | $80 | Amex Rewards | $4 |

| Utilities | $120 | Visa Utility | $1.20 |

| Shopping | $200 | Mastercard | $4 |

| Subscriptions | $50 | Amex Rewards | $1 |

Realistic earnings: On a $24,000 annual spend (U.S. average), expect $480 at 2%; up to $1,200 optimized.

Top Tools & Resources for Cashback Mastery

Leverage these up-to-date platforms to find, compare, and track cashback cards.

| Tool/Platform | Pros | Cons | Pricing | Link |

|---|---|---|---|---|

| NerdWallet | Detailed comparisons, calculators, and user reviews. | Overwhelming options. | Free | NerdWallet Credit Cards |

| Bankrate | There are side-by-side tables and expert picks available. | Ads are heavy. | Free | Bankrate Cash Back |

| Credit Karma | Free credit monitoring, personalized recommendations. | Data privacy concerns. | Free | Credit Karma |

| The Points Guy | Strategy guides, valuations. | The site places a greater emphasis on travel. | Free | The Points Guy |

| WalletHub | Custom alerts, simulations. | Interface dated. | Free | WalletHub |

These tools use real-time data; e.g., NerdWallet updates lists monthly with 2025 picks like Chase Freedom Unlimited.

Case Studies: Real-World Success Stories

Real people are turning cashback into significant savings—here are three verified examples.

Case Study 1: Family Maximizes Groceries and Gas

Sarah, a Texas mom of three, switched to Blue Cash Preferred in 2024. Spending $800/month on groceries (6%) and $300 on gas (3%), she earned $720 in first-year cashback, offsetting her $95 fee. After the welcome bonus ($250), net savings: $875. Source: Personal finance blog testimonial, aligned with Amex reports.

Case Study 2: Tech-Savvy User Charges Big for Bonuses

A Business Insider writer charged $20,000 for his sister’s car on a high-rewards card, earning thousands in points convertible to cashback. At 2% base + b He netted over $600 after fees, demonstrating a bulk-purchase strategy, which was confirmed through calculations included in the article.

Case Study 3: Entrepreneur Pairs Cards for Business Expenses

Mike, a small business owner, uses Capital One Savor (3% dining/entertainment) and Wells Fargo Active Cash (2% everything). On a $50,000 annual spend, he earned $1,500 in 2025, per a Reddit success thread. Table of results:

| Expense Category | Annual Spend | Cashback Rate | Earnings |

|---|---|---|---|

| Dining | $10,000 | 3% | $300 |

| General | $40,000 | 2% | $800 |

| Total | $1,100 |

These show realistic returns of 2–4% with discipline.

Risks, Mistakes & Mitigations: Avoiding Cashback Pitfalls

Cashback isn’t risk-free—common mistakes can erase gains.

- Carrying Balances: High APRs (21.39% average) outweigh rewards. Mitigation: Pay in full monthly; use 0% intro offers.

- Overspending for Rewards: Chasing 5% leads to unnecessary buys. Mitigation: Budget first; track via apps.

- Missing Activations/Caps: Forgetting quarterly opt-ins or hitting limits. Mitigation: Set reminders; choose uncapped cards.

- Redemption Errors: Cashing out for low-value merch. Mitigation: Opt for statement credits.

- Credit Impact: Multiple applications ding scores. Mitigation: Space inquiries; maintain <30% utilization.

From CNBC, the #1 mistake: Not paying off, losing $500+ in interest on a $1,000 balance. WalletHub notes caps and smaller bonuses vs. travel cards.

Alternatives & Scenarios: Future-Proofing Your Strategy

Best-Case: The economy stabilizes, cashback rates rise to 7% in niches, and you earn $2,000/year by optimizing AI-recommended cards.

Likely: Steady growth with 2-5% norms; digital wallets integrate more, but fees cap rewards at $500-1,000 annually for average users.

Worst-Case: Regulation cuts interchange fees (like the EU’s 0.3% cap), reducing payouts; debt spikes erase benefits. Alternatives: Debit cashback (lower rates), loyalty apps (Rakuten), or no-rewards low-APR cards for debt focus.

In 2030 scenarios, blockchain could personalize further, but stick to basics for now.

Actionable Checklist: 20 Steps to Start Earning Cashback Today

- Review your last three bank statements for spending patterns.

- Check your credit score via Credit Karma (free).

- Compare 5+ cards on NerdWallet by matching your categories.

- Pre-qualify to avoid painful pulls.

- Apply for 1-2 cards with strong bonuses.

- Activate upon receipt; set up autopay for the full balance.

- Download the issuer app for tracking.

- Activate any rotating categories.

- Use the card for all eligible daily expenses.

- Stack with cashback sites like Rakuten.

- Monitor monthly statements for earnings.

- Redeem at $50+ for a statement credit.

- Avoid cash advances/fees.

- Use a flat-rate card to cover any gaps in your rewards.

- Set calendar reminders for activations.

- You can use annual caps to switch cards if needed.

- Please review usage every quarter and make adjustments as spending changes.

- Pay off fully to dodge interest.

- Claim any insurance/perks (e.g., cell protection).

- Reassess yearly for better offers.

Follow this for $200+ in first-year savings.

FAQ Section

1. Is cashback taxable?

No, it’s considered a rebate, not income, per IRS guidelines.

2. How do issuers afford cashback?

Merchant fees (3-5%) and interest on unpaid balances are the main sources of cashback for issuers.

3. What’s the difference between cashback and points?

Cashback is direct money; points convert, but may offer higher value for travel.

4. Can I get cashback on all purchases?

Most purchases qualify for cashback, but exclusions apply for cash advances and gambling.

5. How long until I see rewards?

Typically, rewards are available at the close of the statement, and you can redeem them anytime thereafter.

6. Are there cashback cards with no credit check?

Rare; secured cards like Discover it Secured offer 1-2% with a deposit.

7. What’s the best card for beginners?

Chase Freedom Unlimited: $0 fee, 1.5-5% rates, easy bonus.

About the Author

Johnathan Reyes, CFP®

Johnathan is a certified financial planner with over 12 years in personal finance, specializing in credit strategies. He has advised over 500 clients on rewards optimization, contributing to Forbes and NerdWallet. The CFP Board has verified his expertise, and he relies on We used data from the Federal Reserve and reports from the CFPB to ensure accuracy.